| eventi | newsletter |

contatti | cerca |

|

|

|||||

|

|

Bibliografia

|

Articles - Essays

1. IntroductionA very detailed study of the Bitcoin [1] functioning is required for a deep comprehension of it. In this dissertation I tried anyway to avoid too technical topics or subjects being not functional to the established objectives. Paragraph 3, after a brief historical overview, synthetically explains what Bitcoin is and how does it work. Readers already aware of these features can jump directly to the following paragraphs. Anyone willing to go deeply into the technicalities can find in the addendum all the details concerning the implementation of the Bitcoin protocol and of its pivotal points (mainly cryptography, digital signature and other IT concepts) [2]. 2. Historical overview

Fig. 1. The libertarian and anarchist Bitcoin vocation also emerges in some of his imaginative representations although detectable in the network. In the lemniscate the maximum number of bitcoins in circulation. Below the sentence "in cryptography we trust".

Bitcoin historic roots can be dated back in 1982, when the first germinal description of a cryptographic and untraceable means of payment appeared, edited by David Chaum, a computer engineer specialized in cryptography. From a re-elaborated and extended version of this draft, Chaum himself realized in 1990 a first working implementation of the system he conceived, denominated eCash. But the concerns of the Californian engineer were not circumscribed to mere technical aspects. He also encouraged discussions and confrontations about such issues as anonymous digital currency and reputational systems [3] based on pseudonyms, concurring to make the surrounding environment an optimal incubator for further fruitful developments. So then in the early ‘90s different groups supporting cryptography as a means of social and political change started to operate, mainly in Silicon Valley. In 1992 the chyper-punk [4] movement was founded, congregated around a mailing list in which technical issues concerning cryptography, mathematics, informatics as well as philosophy, politics, privacy and more were discussed. One of the founders of the movement was Timothy (Tim) May, who spent a lot of years working as electrical engineer for Intel where, as chief of the research department, solved problems of a certain importance in the field of integrated circuits reliability. May, during the most engaged years of his activism – from early 90’s to his retirement in 2003 – shaped the movement in a peculiar way, concurring to build an ideal bridge between the universe of cryptography and anarchism, that is Crypto-anarchism, sort of a virtual place in which the principles of anarchism can be realized. May consolidated the conceptual side of the movement by redacting, in 1992, the Crypto-Anarchism manifesto, followed in 1994 by the “Cypernomicon”, an outright summa of the theoretical chyper-punk principles. May was insofar sure about the enormous impact that the cryptographic digital technology would have had on the social structures in a very near future, to estimate it to be of the same relevance as the one brought in by the invention of printing:

To fully understand these statements of May we should consider that cryptography and digital protocols not only support reserved informations exchange – of which currency can be seen as a peculiar specialization – but can also get to implement stipulation, audit and respect of sheer contracts between anonymous contractors, independently from third parties, government or assimilable. May himself considers Crypto-anarchism to be somehow a variant of Anarcho-capitalism, a political philosophy promoting individual sovereignty within a liberal market from which the State has been definitely banned. The theoretical foundations of this mainstream of thought can be led back to the person, moreover controversial, of Murray Rothbard and to the austrian economic school in general. As we will see afterwards, this ligature of thought shall re-emerge when we study the creation of currency in the Bitcoin system and its peculiar deflationary behaviour. On the road leading to Bitcoin we find, in 1998, an article written by Wei Dai describing a system “using peer to peer networking to enable payments within parties without relying on a mutual trust”. Clearly influenced by the work of Tim May, Wen Dai started his paper as follows:

Wei Dai’s “b-money” almost contains the entire framework of the protocol on the bases of which Bitcoin has been implemented shortly afterwards. In 2008 a developer known as Satoshi Nakamoto – still is not clear if this is a nickname and if a group of people are behind it – edited the white book of Bitcoin protocol [7]. On January 3rd 2009 the first Bitcoin network was born and the first coins were generated. After the first unstable steps hallmarked by reliability problems, Bitcoin quickly starts to be talked about, within further downfalls – such as the close-down of Silk Road, a web site selling drugs using Bitcoin as currency - , speculative bubbles and blatant announcements of openings or closures coming from governmental agencies or big business corporations. In April 2013, the Bitcoin economy exchange has been evaluated over 11 bilion dollars. 3. Synthesizing BitcoinBitcoin is a crypto-currency, that is an electronic currency based on cryptography (denotated as BTC or XTC) – implemented in 2009 by a not clearly idendifiable developer hiding himself behind the nickname Satoshi Nakamoto. The Bitcoin protocol – whose specifications Satoshi Nakamoto engineered in 2008 – contemplate transactions between users of a not hyerarchized net of computers whose hosts are functionally equal amongst them. [8]. The peculiar configuration of the Bitcoin protocol implicate the needless of third authorities granting the validity and substantiality of the transactions. In order to achieve this goal, each Bitcoin net user must keep on his computer an updated copy of the record covering all the transactions so that they can be of general public knowledge. Each user of the net stores the Bitcoin in an “electronic wallet” resident on his computer or care of a third and qualified institution. The money is transferred by means of encrypted transactions amidst public addresses not refearable to any identifiable individual. Albeit public the transactions are de facto anonymous. The protocol itself preserves the users from the eventuality that other malicious ones can spend two or more times the same coins appointing to the single hosts of the net the task of validating the fulfilled transactions. This “job” is paid by the Bitcoin protocol with a predeterminate amount of Bitcoin, halving every 4 years (currently 25 BTC are being paid). In the Bitcoin slang this operation is known as mining.In 2140, as the last mining activity has been done, the remuneration of the “extractive” activity will be zeroised, while the bulk of circulating Bitcoin will reach its maximum peak (21 millions BTC). From that moment on the Bitcoin users, in order to stimulate the validation activity of hosts of the net, will be asked a small commission for each executed transaction. 3.1 How to use Bitcoin

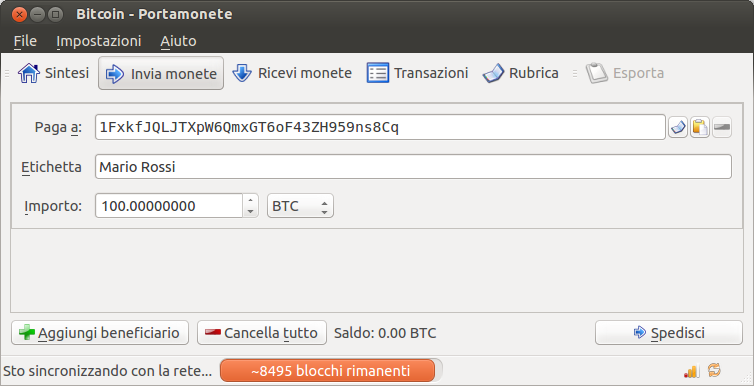

Fig. 2. Client Bitcoin

The first step for using Bitcoin consists in getting hold of the so called wallet, which allows admittance to the Bitcoin net and starting to carry out transactions.The wallet permits the generating of the public addresses that, in the same way of email addresses, enable to get and to send money. Different typologies of wallets are available: software, smartphone or web. The first ones are programs addressed to one’s home pc and are available for the most widespread Operating Systems (Windows, Mac and Linux). A wallet software by now “classic” is the original client Bitcoin engineered by Nakamoto (see fig. 2) but others are as well available, offering several additional functionalities. Smartphone wallets must be installed on one’s mobile telephone and allow to ease QR code payments. Finally, web wallets enable to manage the single addresses through third websites, simplifying the overall management by being easily accessible both by user’s home personal computers and smartphones. Each kind of approach offers advantages and detriments, about which we won’t moreover dilate. In order to start using Bitcoin is first of all necessary to get oneself some Bitcoins. There are three ways to do it:

Now, let’s assume that we bought some Bitcoin from a qualified website. We then can transfer the money to an address of our own after generating it through the Bitcoin wallet in a couple of clicks. This address unequivocally identifies us as addressees of a Bitcoin transaction, as an email address would do. Coming as a dumb sequence of alphanumeric scripts, is proper to assign it a label in order to remember its adhibition (for instance “Donations” for identifying the address due to receive them if we are a no profit organisation). The security best practises suggest using a different address for each different transaction, the address being actually the public side of a couple public key-private key of the asymmetric cryptography. The private key is used for digitally signing our Bitcoin transactions, in practical terms for having them disposable and to publicly attest being the active holders of a certain public address, but the wallet, in spite of arising with a rather intuitional interface, does hide the implementative complexities. Let’s now go trough the simple steps to fulfill to complete payments. After opening the suitable frame of the wallet (check, for instance, fig. n.2 showing the case of the original client) all the required fields, such as the consignee address (usually this will be the case of a cut and paste from the recipient site rather than the acquisition of the QR code via smartphone) must be fulfilled; then a label for a “spoken” identification of the transaction has to be applied (e.g. “Books purchase”, optional but suggested). Finally, of course, there is the total amount. Once the send button is clicked the transaction is widespread trough the whole Bitcoin net which keeps it in a temporary abidingness state until the final the operation is officially confirmed by the net itself (usually within 1 hour). It’s also possible to create transactions with multiple recipients by censusing each one of them in the appropriate frame. After clicking the send button the wallet will choose, following a certain algorithm, the address from which withdrawing the available Bitcoin (should different receiving addresses be available). Actually, the addresses are not the exact counterpart of a bank account, so they are usually not enclosed with the transactions, in order to grant the namelessness of the involved actors (I can’t have knowledge of who I got a certain amount of money from). Is more correct to relate the concept of bank account and of total balance to the whole of the addresses stored in a wallet. This is, indeed, also the balance displayed by the main screening of the Bitcoin client. Additional functionalities are an address book, a filtrable list of the executed transactions and a screening for the user to sign with his private key a certain message, useful for proving to actually being the owners of a certain public address. Apart from this last functionality, this is a very simplified version of what is normally found in the home banking application program interfaces bynow offered to every bank account holder. Special attention must be addressed by the Bitcoin user to wallet protection. As previously mentioned, the private keys are what needed for demonstrating the paternity of a certain amount of Bitcoin. Losing them would mean hopelessly losing all the money. Thus it’s essential adopting several security precautions contemplating at least the wallet encryption and a periodical backup of the wallet itself, that is the record of the private keys. Presently there is no evidence of any company or institution disbursing Bitcoin loanings. After all, as we will see in the following pages, embodies mechanisms based on smart contract that allows fund raisings by means of “digital subscriptions” launched on the net. 4. The dark side of BitcoinIn this chapter we will try to highlight the vulnerabilities of the Bitcoin protocol. However, contrary to what one might immediately expect, the topic of the discussion here has nothing to do with issues of information security, namely flaws in the protocol that may affect operation and hence credibility. It is widely known that the effectiveness of hacker attacks goes hand in hand with the progress of computer sciences in designing increasingly safer and more secure systems. In principle, hackers could definitely bring down the entire Bitcoin system rather than simply opening up gaps of differing size here and there if they were to go a step too far. It could also be argued at length about the likelihood of such an event occurring. However, as important as the issue of security may be, in our opinion, it is secondary so we are glad to leave this aspect to the software's ordinary evolution and improvement processes. The vulnerabilities, or rather the intrinsic and structural weaknesses, of the Bitcoin Protocol that we will be discussing regard mainly two aspects that are somewhat related to one another. The first to be illustrated is linked to the creation of money. 4.1 A limited money supply The remuneration of mining is the only way to create new bitcoins. Certainly those who created the Bitcoin protocol had to deal with an all but trivial problem, namely allowing peer-to-peer network users to create money while avoiding that inflation could arise from this generation activity. If every node in the network were allowed to issue currency at will, the experiment of a crypto currency would not even be worth trying. In Bitcoin's case, the problem has been solved in a brilliant way by linking the issue of currency to an actual activity, the so-called proof of work. The idea itself is sound. The remuneration of the validation process carried out by the nodes in the network represents the fair compensation for the service provided, exactly as if you were to request it on the market. You get money in return for the hours or days of computing. It is an easy calculation. This original way of issuing money though has a problematic consequence: the total amount of currency in circulation is limited, hence expansionary forces will eventually drive the system to deflation. In the Bitcoin wiki, the deflation issue is discussed under various topics. The following quote somehow summarizes the "official" position:

If it is true that a classical economist typically has a sort of deflation horror vacui, there is no doubt though that the worst financial crises have been precisely those having a deflationary nature. It is also questionable whether the Austrian school of economics has actually managed to have the last word when it comes to this issue despite its many positive theoretical contributions. The same Bitcoin wiki mentions several authors out of (its) chorus and several debates have ensued on the Web suggesting that the issue is still open or at least that is rather risky to consider the future deflationary behavior of Bitcoin as being certainly advantageous. 4.2 The possibility of accumulation

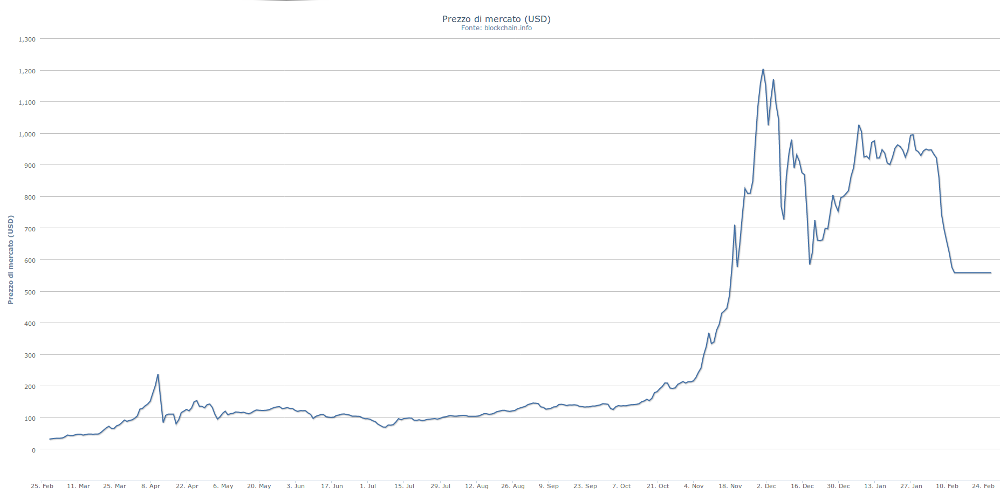

Fig. 3. Trend of the market price of Bitcoin from February 2012 to February 2013 in USD (source blockchain.info).

To introduce now what we have identified as a second vulnerability of Bitcoin, let's consider on the one hand that the possibility of spending bitcoins is now somewhat limited - suffice it to look at the list of companies all over the world that accept bitcoin payments - and on the other hand that the value of the Bitcoin economy has already exceeded USD 6 billion (November 2013). In such a context, it should be no surprise that an interesting quantitative analysis of Bitcoin transaction concludes that "most of the minted bitcoins remain dormant in addresses which had never participated in any outgoing transactions." [10]. The debates that have ensued in the Web around this analysis seem to be quite interesting and symptomatic: Several supporters of the crypto currency argue that if this primarily speculative interest in Bitcoin should just be considered a bad thing, well, it is a necessary evil in order to allow the extensive spread of the crypto currency. They also note that, similarly to traditional legal tender currencies, Bitcoin also serves the function of a reserve of value that can be hoarded and this is considered as an element in favour of the crypto currency. The reader might well be surprised now that a trait that Bitcoin shares with the other traditional currencies is classified as a vulnerability. The reason will become clear, however, further in the discussion. For the time being, let's consider how all of this is nothing else than the litmus test of how Bitcoin is a currency projected towards the future but that shares many of the aspects of traditional currencies from which it intends to distance itself as their revolutionary alternative. However, it is not our intention to be unfair toward Bitcoin, which indeed appears to be a grand edifice of thoughts and ingenious solutions. But to allow it to effectively fulfill its libertarian vocation, it must necessarily evolve by making another conceptual break from traditional currencies going to the root of the economic thought from which it draws its origins. 5. The perishable currency of German anarchismIn the historical introduction we highlighted how Bitcoin is rooted in crypto-anarchism that developed, starting in the 1980s, mainly thanks to activists from the departments of electronic engineering and computer sciences on college campuses in California. The intuition of the potentially revolutionary scope of cryptographic techniques in the form of virtual communities inspired by libertarian principles ideally had opened the doors of the world of anarchism to the activists of this movement. However, when speaking of anarchism, it seems that the crypto-anarchists have taken the anarcho-capitalist figure of Murray Rothbard and other members of the Viennese school of economics as their theoretical reference without establishing a contact with the economic concepts that developed in European anarchism in the early 20th century and had a certain resonance in the United States as well. 5.1 Silvio Gesell and Schwundgeld In the 1930s and 1940s at least fifteen complementary currencies spread in the United States and in Canada. These were modeled on Schwundgeld, literally "money than fades", also known as "stamped money", created by Silvio Gesell and launched in Austria in 1936 in the famous "Wörgl experiment". Even the well-known American economist Irving Fisher who had recognized the value of the idea of monetary de-cumulation or demurrage praised and promoted American versions of Gesell's currency. Without dwelling on a theoretical discussion of demurrage [11], the mechanism of de-cumulation developed by Gesell, in brief, consists of a tax on liquidity payable periodically to the state as a "stamp" to be placed on the back of the paper currency to maintain the nominal value unchanged. After the expiration date of the reporting period - for example, every month for an amount of 1% of the face value - a bill without the stamp would have no value. The tax could also be collected in other ways such as through automatic taxation of checking accounts or in other ways. To avoid paying the periodic tax, holders of money are therefore encouraged to keep as little money as possible. The flow of money that is generated is used by the state, which typically will use it for public investments to achieve full employment. Monetary de-cumulation puts therefore an end to the stagnation of capital in the economic body. To use an image, it is as if in the latter the 'temperature' started to increase and the 'frozen' monetary financial assets started to melt and flow; annuities that clogged the unproductive economic fabric would be dissolved and, driven by the increased velocity of cash circulation, it would seek outlets in the form of new investments which in turn would generate additional employment. However, Schwundgeld, at least as originally formulated by Gesell, does not prevent the speculative behavior of economic operators, shows a marked propensity to generate inflation and, above all, does not adequately address the problem of credit, namely of how new money is generated. From this point of view Gesell's positions were rather traditional and could not imagine anything but the 'usual' central bank that issued currency under a monopoly on behalf of the state. Therefore, there is a need for a revision and an evolution in Gesell's scheme, which can be found only in the social thought of the Austrian philosopher Rudolf Steiner. Much less known than Gesell and almost unknown in anarchist and libertarian circles despite his bonds with German anarchism [12], in the period following the First World War, Steiner conceived an innovative monetary reform as part of a broader and more complex social reform that he called "the threefolding of the social organism". 5.2 The evolution of Schwundgeld: Purchase money, gift money and loan money In the Steinerian circuit, Gesell's scheme needs two substantial changes [13]. The first of these concerns the social actor tasked with the collection of the "stamps", namely the final recipient of monetary de-cumulation. In keeping with the functional separation of the economic, cultural and state domains specific to Steiner's social tripartite division, de-cumulation should not be managed by the state. Indeed, the state must be completely excluded from the economic sphere. It must limit itself to enforcing laws without direct intervention in economic life. In Steiner's system, monetary de-cumulation should instead be channeled to funding the cultural sphere of the social organism, which is made up of all those institutions that belong neither to the state nor to the economic sphere: hospitals, schools, cultural foundations, theaters, universities, etc. namely everything that typically represents a cost center, the uneconomic element of society. In order for de-cumulation to reach a given cultural institution rather than another depends on the free will of those who have to pay. When I pay the "stamp", I also decide who to donate the amount to. In this way, it is possible to build up a free social cultural life in the social organism founded on it and independent of both the state and the economic sphere. The function of redistribution no longer lies with the state sphere and is placed in the hands of civil society, in accordance with the libertarian nature of threefolding social order. De-cumulation affects the entire currency in circulation, but it is possible to preserve savings from its effects by handing it over to banks, which, in order not to incur the stamp costs, will invest the money accordingly. For the depositor the consequence is that of being able to "freeze" savings at the date of the deposit and to delegate the burden of de-cumulation to others. Steiner thus distinguished the currency that we use routinely as a means of exchange and which he calls purchase money from that originated from de-cumulation: gift money or "old money". It is important to emphasize that the concept of gift money does not have any moral connotation in the Steiner's scheme, as it has a specific economic function. The second change to be made in the Schwundgeld scheme regards the fact that it tends to be inflationary due in part to the increased speed of movement and to a greater extent to the fact that it continues to be issued by a central bank orbiting around the state sphere. In fact, Gesell completely missed a fundamental aspect of currency which is manifested through the creation of investment banks. This is a phenomenon that did not go unnoticed by Joseph Schumpeter, he too connected in some way to the Austrian school of economics, who in "The Theory of Economic Development" of 1911, identified the dynamic element that could lead a stationary system - like Gesell's system - to make the quantum leap capable of assuring new growth and progress, "an innovation no less powerful than electricity to explain the second industrial revolution" as the economist Aleksander Gerschenkron later said. For Schumpeter, like Steiner, the decisive factor that allows a system to abandon a steady state is credit, which should not be understood as a mere collection of "purchase money". It is a type of money other than that which is normally used to exchange goods and services. And yes, he did refer here to goods and services, but not current ones, but future ones, those that will be implemented through a business venture or through a transformation of existing processes carried out for example by a qualified technician. In general, as regards the highest results achieved in the transformation of labor by the Spirit, that is to say by individual talents and skills. The money that is used for this purpose has no ties to the current mass of circulating capital, concerning as it does its link to future goods and services alone which it has the power to give rise to in the future. Its justification must be sought not in the present but in the future needs of the community which should be planned today. Steiner called this investment money loan money or even "young money". It is the monetary instrument that is made available to entrepreneurs so that they can fulfill their creative function of value while the issuing or investment banks are social actors responsible for its provision. Proven management skills and personal credit understood as a solid reputation and reliability, are the guarantees that these banks ask from the entrepreneur. In the hands of talented entrepreneurs, loan money brings into existence new economic realities, hence transforming into spending power for households through wages, through the payment of suppliers, etc.; it slowly becomes purchase money which in turn becomes gift money. Through the spending of cultural institutions, gift money returns to businesses and then to the issuing banks that destroy it without harming the monetary balance of the system. It should be borne in mind though that the three kinds of money are not physically distinct. They are the same currency that takes on different functions depending on how close or far the de-cumulation is. The issuing of loan money, as clarified by the economist Geminello Alvi, lies with the issuing banks operating under a free banking system. That means not a single central bank, but several issuing banks in competition with one another and this is what keeps Steinerian monetary circulation from experiencing inflation. Steiner's scheme is completed by a further reform of financial markets in order to limit speculative behavior to a maximum and introduce economic associations to allow banks to better calibrate their investments. By bringing together representatives of producers, consumers, traders and goods carriers, economic associations would be tasked with providing the credit system with the elements needed to properly assess the financing of only those products that are intended to cover the actual needs of the community. 6 Towards a new three-in-one crypto currencyLet us now try to describe the changes to be made to Bitcoin - or to be made by a new crypto currency derived from it - to address at least some of the issues examined above. Clearly these are just hints and hypotheses to be further developed. First, we must point out that there already is - among the countless cryto currencies that are popping up like mushrooms - a fork in the Bitcoin project that implements Gesell's de-cumulation scheme called Freicoin. 6.1 Freicoin Freicoin is a crypto currency that implements Gesellian de-cumulation by making a change to the Bitcoin protocol from which it derives. The rate of decumulation is currently set at around 5% a year. However, there is no way to direct de-cumulation to any beneficiary of one's choice; the levy is in fact carried out automatically. The introduction of de-cumulation necessarily involves a review of the mechanisms that generate new currency in Bitcoin. In this regard, the creators of Freicoin first argue, not without reason, that although the activity of miners is essential to ensure the security of transactions, it is not necessary to consume large quantities of real goods - electricity, hardware, etc. - to issue 100% of the currency. In Freicoin it is therefore expected that only 20% of the total money can be generated through mining. The remaining 80% is immediately created and put entirely at the disposal of a non-profit organization created ad hoc, namely the Freicoin Foundation whose mission is "to create a world where commonplace non-usurious complementary currencies inspired by the works of Silvio Gesell are brought into being through economic development, charitable action, and the support of global commons and which engender perpetual prosperity through sustainable development". The Foundation has the task of distributing its available funds within the first three years of life of Freicoin (distribution should be completed in 2016). After this period, a finite money supply amounting to 100 million freicoin will have been generated. Freicoin marks a return to centralized issue but the Foundation, in the plans of its creators, should be transitional. The objective is undoubtedly to make Freicon a completely peer-to-peer and decentralized currency but not without identifying effective mechanisms that enable it to put the money issued to use in accordance with the Foundation's mission. It will be possible to release Freicoin from central issue only if a solution were to be found to these problems:

This gives rise to a particularly arduous dual challenge: Freicoin should, on the one hand, make the management of donations similar to that of complementary currencies such as the Chiemgauer [14] and, secondly, find an efficient solution to the problem of creating new money. All this without resorting to "central agencies". 6.2 A proposal: bitmercor, bitdonor e bitinvor It is likely that the solutions to the above problems are difficult to find until you search for them in a single system. But Steinerian monetary circulation, as described in the previous paragraphs, may perhaps provide the key to a broader scenario within which Freicoin can evolve. The currency that circulates in Bitcoin-Freicoin is in fact what Steiner calls purchase money, namely money to be used as a pure medium of exchange. We will call bitmercor [15] the functional domain that originates from the circulation of this currency. It is the functional domain of the pure exchange of assets and the current operation of the Bitcoin protocol is sufficient for this purpose. Clearly, even the ordinary monetary circulation of Freicoin is bitmercor but, with de-cumulation, it implicitly introduces another functional domain that we will call bitdonor. This domain is responsible for regulating the allocation of demurrage, but it does so with its own rules that may require the introduction of a new protocol, which is different from that of Bitcoin-Freicoin. Bitdonor as an expression of civil society understood in the sense of Nicanor Perlas, or as a third social pillar alongside the state and market pillars, should deal with:

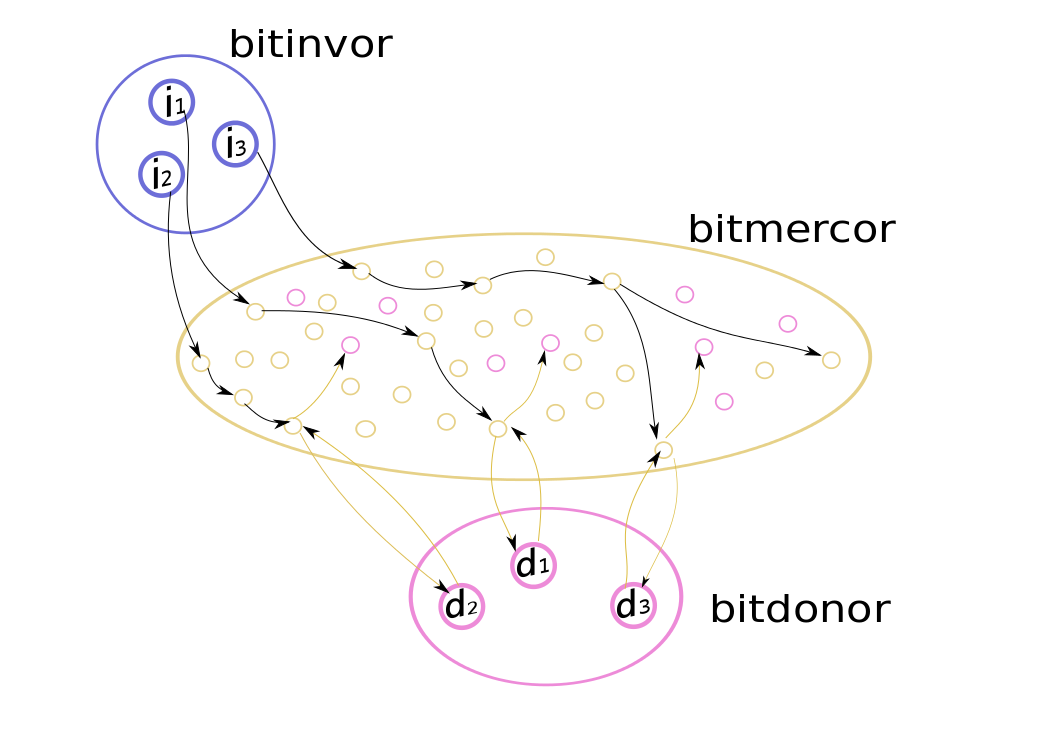

Fig. 4. The bitinvor domain comprises entities (i1, i2, i3...) that manage the issue of credit to finance new businesses. The money flows into the bitmercor domain and becomes purchase money. Demurrage is forwarded to cultural institutions subject to verification with one of the public registers d1, d2, d3 of bitdonors that the recipient is an accredited cultural institution.

Bitdonor could also be organized as a peer-to-peer network and adopt a Bitcoin-like protocol to implement the tasks requested of it. For example, the generation of the public key that identifies a given cultural institution could be the result of a process of gaining a certain level of consensus, after which the institution may be considered accredited. The mechanism to check already registered institutions could avail itself of a reputation-based system that assigns a certain percentage of "ethical reliability" to the accredited institution. Below a certain threshold, the institution may be automatically excluded from donations, either temporarily or permanently. Finally, to economically support bitdonor in its institutional tasks, a portion of the donations can be reversed to cover expenses. But how should bitmercor interact with bitdonor? The Bitcoin protocol supports the implementation of smart contracts. Of these, an example is provided in Bitcoin's documentation. It describes the query of an oracle, i.e., an external system that is able to respond true or false to a request made by a Bitcoin transaction. The oracle's answer is binding for finalizing the transaction successfully. Therefore:

The bitmercor circuit should also make sure that donors can be spent once and only once and only by users registered with bitdonor, that is, that they are cultural institutions and not other entities. The above considerations should address the first of the two issues that Freicoin should solve. Now the complex issue of monetary emission is to be addressed. Maybe the reader may have noted that the difficulties typical of the bitmercor domain are usually due to basically technical or other problems which can be solved through automatic electronic processing. This was finally the nature of the problem of the validation of the Bitcoin block chain. But the bitdonor domain already starts to deal with issues that are not easily manageable through mere IT solutions. Assessing whether a cultural institution meets the requirements to access donors may be the result of an IT process but it requires a well-defined institution rather than a peer-to-peer network. This is even more true with regard to the issue of money. We have seen in the section on Steiner's evolution of the Gesellian scheme that the issuing of currency is managed by different issuing banks in a free banking scheme. Today, the banking system is the subject of harsh criticism which rightly stigmatizes the all too cynical and unscrupulous conduct of institutions that have completely forgotten their social function and are deformed under the weight of the exasperated search for profit maximization. But you cannot think of throwing the baby out with the bathwater. The issuing banks should act as a sort of organ of social perception in the search for skilled entrepreneurs to whom to entrust the credit needed to anticipate the future creation of goods and services. It is an important and delicate function that requires extensive experience and specific skills that are unlikely to be substituted by a peer-to-peer network of heterogeneous subjects who lack the necessary skills. At present, it is frankly difficult to adequately address this issue without presupposing some sort of replica of the banking function to deal with the issue of loan money to businesses. If we call this functional domain bitinvor (see Fig. 4), it should rely on various institutions operating as banks. An appropriate change to the Bitcoin-Freicoin protocol should allow bitinvor institutions to grant the amount of funding to an entrepreneur ex nihilo, exactly as is the case today when the protocol pays miners. In accordance with the tenets of economic associationism in Steiner's tripartite division of society, entrepreneurs should produce only the goods actually required by the community to which they belong. This has two positive consequences: a significant reduction of business risk on the one hand and, on the other hand, an appropriate sizing of its production capacity. The bitinvor domain should then interact with economic associations to be able to optimally finance only those firms dedicated to meeting the real needs of the community. In this regard it is possible through a peer-to-peer network to make sure that the associations of consumers and producers can express and quantify their needs in some way. For the disbursement of funding, the relevant transaction could then be finalized with a smart contract only if the following conditions are met:

7. ConclusionWe have highlighted the anarchist and libertarian roots of Bitcoin's genesis and its role as a means of exchange for mutually cooperating subjects in anarchist communities in which the state is entirely absent. The path that Bitcoin has so far taken to achieve the purpose for which it was born is characterized by solutions that can be considered brilliant. The overall design of its implementation starts to reveal part of the mystery of what currency is and to manifest its ethereal, intangible nature, essentially based on human trust. But this process of 'monetary epiphany' has not come full circle yet. Light has been shed on how the theoretical roots of the libertarian principles inspiring Bitcoin delve into anarco-capitalism and other currents of contemporary liberal and anarcho-individualist political philosophy. All this has greatly influenced the design of Bitcoin which has focused primarily on the need to exclude the state from the economic sphere. But in doing so, it has neglected to investigate the real nature of money. Aside from this, Bitcoin risks ushering the ills of today's money into the anarchist communities of which it aspires to become the means of exchange, thus contaminating electronic money. Yet it was precisely in circles contiguous to anarchism where the concept of monetary de-cumulation was initially developed through the thought of Silvio Gesell. It was then perfected as part of the complex transformation into the threefolded social organism conceived by Rudolf Steiner, he too connected to German anarchism. It postulates "loan money", "gift money" and "purchase money", each of which becomes the other as part of a cycle similar to that of blood in a living organism. Freicoin is a crypto currency derived from Bitcoin that natively implements Gesellian demurrage. It could be the starting point for an implementation of Steiner's three kinds of money, which, as illustrated in the previous chapter, are focused on three separate functional domains: bitmercor, bitdonor and bitinvor. Here it is important to note that Bitcoin and other crypto currencies derived from it have various mechanisms (proof of work, reputation, smart contracts, etc.) which can at most support majority decisions in the context of virtual communities based on peer-to-peer networks. But as said, especially the process that leads to the generation of money is far from being comparable to a democratic process. The bitdonor and bitinvor domains almost certainly require centralization and it is mindless to force them into mechanisms that are foreign to them solely to comply with an abstract requirement of anonymity. The exclusion of the state from economic sphere is much better achieved when money can actually be guaranteed an independent genesis as investment money and its subsequent transformation into purchase money and gift money with modalities typical of each functional domain. Rather than attempting to spread an electronic currency that is in general invisible to the state, it is more appropriate to create the conditions for healthy monetary circulation within small communities where you have the market, cultural institutions and entrepreneurial skills in search of the credit needed for the production of the goods and services required by the community. By creating the conditions for its circulation, much will have been done to allow the new currency to firmly take root in a given territory and to give rise to new economic processes independent of the state sphere. The hurdles to overcome in order to integrate Steiner's three kinds of money into a crypto currency may seem huge. In the 1980s and 1990s, the difficulties strewn along the path ahead of David Chaum, Tim May and other pioneers of crypto-anarchism definitely appeared to be no less formidable. Yet, less than thirty years later, the whole world has seen the Bitcoin phenomenon in all its magnitude and this is just the first implementation of crypto-anarchism! What is essential now is to head in the right direction. Notes:[1] Following an agreement by now fairly widespread in the network, 'Bitcoin' (capitalized) refers to the protocol or the concept in general, while 'bitcoin' (with an initial lowercase) refers to the single instance or the 'physical' money. [2] For a complete discussion you can refer to the documentation "official" protocol: https://en.bitcoin.it/wiki/Main_Page [3] From Wikipedia: "A reputation system computes and publishes reputation scores for a set of objects (e.g. service providers, services, goods or entities) within a community or domain, based on a collection of opinions that other entities hold about the objects". A concrete example is constituted by eBay. [4] Perhaps one of the most famous followers of the movement is Julian Assange of Wikileaks. The term should not be confused with cyber-punk from which it jokingly derives. [5] Tim May. Cyphernomicon, 1994. http://www.cypherpunks.to/faq/cyphernomicron/cyphernomicon.txt. [6] Wei Dai. b-money, 1998. http://www.weidai.com/bmoney.txt. [7] Satoshi Nakamoto. Bitcoin: A Peer-to-Peer Electronic Cash System, 2008. http://bitcoin.org/bitcoin.pdf. [8] That is, each node can act as both as a server and as a client, by sending and receiving data according to the needs. Such a network is also known as peer-to-peer or P2P. [9] Paragraph "Deflation" in: https://en.bitcoin.it/wiki/Controlled_supply. [10] Dorit Ron and Adi Shamir. Quantitative Analysis of the Full Bitcoin Transaction Graph. Sito web, 2012. http://eprint.iacr.org/2012/584.pdf. [11] For a more comprehensive treatise: http://www.tripartizione.it/articoli/perishable_money_09_2013.html. [12] For a complete discussion of the relationship between Rudolf Steiner and German anarchism: http://www.tripartizione.it/articoli/GGPreparata_Perishable_Money_in_a_Threefold_Commonwealth.pdf. [13] The innovation of Steiner on the Gesell's schema, a theme extended and somewhat complex, will be discussed here only partially and in a manner consistent with the objective that we have set. To know more about the three kinds of money of Rudolf Steiner, consult the work of economist Geminello Alvi see: L’anima e l’economia. Mondadori, 2005; La Confederazione italiana. Marsilio, 2013; Il Capitalismo - Verso l'ideale cinese. Marsilio, 2011. [14] Recent partial implementation of the money at maturity Steiner, see section on the Chiemgauer in http://www.tripartizione.it/articoli/perishable_money_09_2013.html. [15] We recall here the terminology of the economist Geminello Alvi for which mercor corresponds to the Steiner purchase money, donor corresponds to the gift or old money and invor corresponds to loan or young money. |

|||||||||||||