| eventi | newsletter |

contatti | cerca |

|

|

|||||

|

|

Bibliografia

|

Articles - Essays

“O blessed money, which not only gives to the human race a useful and delightful drink, but also prevents its possessors from yielding to infernal avarice, for it cannot be piled up, or hoarded for a long time!”

IntroductionDrawing an organic theory of value and money from Steiner's cycle of fourteen lectures "The National-Economics Course" and from the six seminars held in July and August 1922, that is the entire body that Rudolf Steiner left us as further considerations on the ideas presented in his Central Points of the Social Question is no easy task. The topic that probably suffered the most from an almost aphoristic approach vis-à-vis a systematic and structured study of these issues was probably the theory of money, which postulated not one, but three kinds of money, each of which transforming into the other through a life cycle that is also not easy to grasp immediately. It has already produced quite a bit of confusion in those who are zealously trying to develop their thoughts in the footsteps of the Austrian philosopher. Now, as then, mainstream culture and academia continue to show no interest at all. In recent times, however, excellent contributions have been made by Hans Georg Scheppenhäuser[1] and Udo Herrmannstorfer, but it is thanks to the insights of the economist Geminello Alvi and other scholars close to him that these issues have finally been deservingly and rigorously revisited in a sort of restoration that has cleared the work from artificial misinterpretations and revealed the true colors of the imaginative power of Steiner's thought. Geminello Alvi addressed these issues in several papers, the first of which was published in the magazine "Trasgressioni" in January-April 1997. Later they were taken up again and published in his other books [2].In the meantime we hope that academics and mainstream economists may find interest in Alvi's theories. In this paper we will focus mainly on Steiner's theory of three kinds of money in an effort to make it accessible to laypeople. However, it will follow Alvi very closely but any differences will be duly highlighted. While with regard to the theory of value, reference should be made by readers to Alvi's works without trying to present here a summary that would lack its rigor and completeness. As for the theory of money, some benefit vis-à-vis the original treatment could be derived from focusing more on some examples and assessing what concrete steps in recent times can be traced back more or less explicitly to the concept of de-cumulated money. A bit of historyUsually, among those who are acquainted with him, Steiner's idea of money usually evokes the concept of the de-cumulation of money, that is that over time it cannot be accumulated, but on the contrary it actually decreases. Technically speaking, it is subject to a negative interest rate. This concept of monetary de-cumulation however is not an invention of the Austrian philosopher. In fact, if you look to the past, this concept has always existed until relatively recently at least at an instinctive level. In the ancient Jewish world, just as an example, Mosaic law prescribed the jubilee. "Seven times seven years" during the jubilee year the entire social body would join in forgiveness. Its economic effect included the restitution of land to former owners and the remittance of debts. The jubilee was hence the instinctive remedy that Israelite society had found to prevent the social harm resulting from an indefinite accumulation of wealth. In ancient Greece, however, in some poleis, the de-cumulation of large fortunes would be achieved through the practice of having the richest families fit out the triremes necessary for the defense of their city-state. Even the Middle Ages had mechanisms for the de-cumulation of money. Odono Por, a little-known Hungarian economist active in Italy in the 1930s, described these with the following words:

Only in the early decades of the twentieth century was the concept of the de-cumulation of money clearly expounded. When Steiner wrote about it for the first time in 1919 in "The Central Points of the Social Question", it had already appeared on at least two previous occasions. It was mentioned the first time by an almost unknown economist, Francesco Avigliano from Potenza, who spoke of a "prescriptible" or "transient" soft money in his book "Perché c'è la miseria?" (Why is there poverty?) dated 1905 [4]. The second time was in 1916 in the book "The Natural Economic Order". The author was a truly unique figure who still enjoys a certain popularity in economics that is definitely much greater than that of the Austrian philosopher. His name was Silvius Gesell. Silvio Gesell

Gesell, sensing the scenario that was taking shape, sold his company to repurchase it later at bargain prices. Suddenly he became rich while the entire Argentine economy plunged into the abyss. What he had just pulled off appeared senseless to him. The way the monetary system worked had rewarded him for his speculative transaction, while the real economy was being strangled by the lack of liquidity that remained idle in banks. All this led Gesell to draw the logical conclusions: The economic system does not suffer so much for a surplus that is not shared with workers as Marx argued. It suffered first and foremost for a structural defect that weighed on money as such. Gesell did not intend to question its role as a means of exchange, but its function as a reserve of value. The economist Werner Onken wrote in this regard:

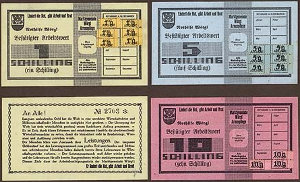

Though lacking rigorous economic studies since he was essentially self-taught - or perhaps precisely because of this - Gesell realized that in the process of exchange of money for goods, the former behaves "unfairly" toward the latter. Money can be accumulated without significant costs and does not perish, while goods, on the contrary, progressively lose their value over time and perishes. If money can be pulled out of the circulation of money for speculative reasons, this violates Say's law according to which every product always has a natural outlet on the market. That is, not contemplating saving, every form of production generates a corresponding amount of income and the latter is always fully spent. Savings are contemplated because at the aggregate level those who spend more than what they earn compensate for those who save. In contrast, Gesell was convinced that withdrawing money from the market for speculative purposes violates Say's Law. His goal was to counter savings in favor of investment and full employment. If the money was to be a fair competitor of goods, then it had to undergo the same process of deterioration. Therefore, it was necessary to tax liquidity in order to drive those who had accumulated money to put it back into the economic cycle. Based on this observation, Gesell elaborated an original reform of money concerning what he called "stamped money". The banknotes of this money, called Schwundgeld (In German: 'geld' means money and 'schwund' derives from the verb schwinden which means to vanish, disappear, and in the past participle becomes geschwunden; so: money that disappears), would show their face value on the front and on the back there would be a grid intended to accommodate stamps to be applied periodically to maintain their validity. The stamps would be issued by the State and could be bought at post offices. The implementation mechanism was simple: to avoid paying this tax on liquidity, the holder of the banknotes could only spend them, thus driving demand and revitalizing the economy accordingly. It was a brilliant idea to quickly jump-start the economies of the countries devastated by World War I. In April 1919, Gesell had the opportunity to put his ideas into practice as the "People's representative for Finance" of the Republic of Bavarian Councils, a short and tragic embodiment of a Soviet republic in the turbulent period following the collapse of the German Empire. Gesell had been called there by Ernst Niekisch, leader of German National Bolshevism and by the anarchist Gustav Landauer. Although Gesell was not in the least a Marxist, the opportunity presented to him could not be wasted even though the situation was chaotic as ever for both the economic climate and the actions of the revolutionary government that committed many mistakes by acting in an uncoordinated and irrational way - the foreign minister, who in the past had had psychiatric problems, even managed to declare war on Switzerland because it had failed to comply with a request of the revolutionary government. But there were also serious attempts at reform and Gesell's stamped money was one of these. But the Bavarian experience proved ephemeral. In a short time the Freikorps sent by the Minister of Defense of the central government in Berlin, Gustav Noske, annihilated Munich's Red Army. The massacre continued with the killing of Landauer and other members of the Cabinet of the Republic of Councils; Gesell escaped the fatal destiny of his comrades only because he was a Swiss citizen. His money, still fresh off the press, had no way to circulate even for a single day... Banned from Switzerland, Gesell, after moving again to Argentina from 1924 to 1927, eventually settled in Germany where he died of pneumonia in 1930 in Oranienburg, near Berlin. He almost had the chance to finally see his reform put into practice, but he died without seeing what would later become known as "the Wörgl experiment":

However, the most famous stamped money experiment in the literature is Schwanenkirken's in 1931, which saw the issue of perishable money called 'Wära', a name composed of words Ware (goods) and Währung (currency, money), whose circulation became frenetic in a short time bringing immediate prosperity to this town, whose fame quickly spread throughout Germany. There were several other similar experiments across Europe, reaching Estonia, where in 1935 the municipality of the town of Ravel issued stamped money amounting to 200 thousand Kronor. Gesell's idea also crossed the Atlantic: its validity was recognized by the famous American economist Irving Fisher, who promoted the emission of stamp script notes in the United States in about fifteen towns throughout the country whose economies were not able to climb out of the Great Depression. He also inspired the American poet Ezra Pound, who found the material to build his own economic theory in Gesell and other heretic economists like Avigliano. In it, labor and money are not commodities, while the only way to eliminate usury from the economic system once and for all was to tax money at regular intervals. It is likely that these events gave Gesell enough notoriety to lead John Maynard Keynes, the iconic figure of economics, to address his work. John Maynard KeynesIt is said that initially Keynes did not want to know anything about Gesell. Critical rants and digressions that abounded in the pages of the writings of the German merchant, together with a not always rigorous form, probably bothered the British economist's delicate sensitivity. Keynes later admitted that "like other academic economists, I treated his profoundly original strivings as being no better than those of a crank." However, he had to admit that there was method in Gesell's madness. Indeed he saw brilliant insights, to the point of saying: "I believe that the future will learn more from Gesell’s than from Marx’s spirit.." He even devoted chapter 23 of his "General Theory of Employment, Money and Interest" of 1936 to the German merchant. In writing about Gesell, he stated:

When speaking of marginal efficiency of capital, Keynes refers to the total amount of future income expected by the entrepreneur (prospective income) for each additional unit of capital including its cost (supply price). In other words, the evaluation of marginal efficiency determines the propensity of an entrepreneur to make an investment: if the prospective costs are low compared to the expected revenues and this ratio is greater than the rate of interest, then the investment is fruitful and should be made. In contrast, high future costs of production mean lower sales and competitiveness, thus less revenue which results in little or no propensity to make the investment. The intermediate case is represented by a marginal efficiency corresponding exactly to the balance between the expected revenues and the rate of interest for which it remains uncertain whether to make the investment or not. In the latter two cases, the operator generally opts for cash, that is he invests in securities on the financial market, which, as Keynes argues, "sets a limit to the rate of growth of real capital" thus damaging the real economy of production means. In the case of a particularly bleak or uncertain outlook for the future, a low marginal efficiency of capital repeated over time can make the entire economic system lapse into the so-called liquidity trap. According to Keynes, this is the situation that occurs if the great majority of entrepreneurs believe that it is inconvenient to make investments in production and opt for liquidity, i.e., hoarding. The resulting decline in aggregate demand leads to recession, and hence unemployment, lower incomes and a further decline in demand in a relentless spiral that leads directly to social and economic catastrophe. Under these conditions, leveraging interest rates is completely ineffective because now, being close to zero, they can no longer exert any pressure on the market - "If something is connected to you by a string, you can move it toward you by pulling on the string, but you can't move it away from you by pushing on the string", Galbraith once said about this issue. Therefore, according to Keynes, the rate of interest is not enough to create a balance between investments and savings and Gesell shared the same opinion. For the latter, interest consists of three components: the first is the remuneration of the risk to which the provider is subject and is considered legitimate; the second is the compensation for losses caused by inflation and it too is legitimate; it is the third that Gesell controversially called a tribute. It represents a "way to store wealth", it is something quite harmful in the economic system and it must be eliminated through radical monetary reform. This is where Keynes' and Gesell's paths diverge or rather appear to diverge. Both are interested in finding that particular value of the marginal efficiency of capital in the economic system that can ensure full employment through productive investments. However, for Keynes this implies a significant recourse to a deficit spending policy, that is public investment in deficit, while for Gesell this is obtained through a new type of money, i.e., stamped money. Putting a stamp on paper money is tantamount to a negative monthly interest rate. Keynes judged Gesell's idea amateurish. Nonetheless, he made the effort to calculate the optimal amount that the stamp should have had: having determined the investment needed for maximum employment, the stamp had to be equal to the difference between the rate of interest and that particular value of the marginal efficiency of capital that leads entrepreneurs toward the overall level of investment, which is the minimum value that discourages hoarding. To understand Gesell's de-cumulation mechanism, let's consider the following calculations (Tab. 1).

Initially, the central bank issues 100 units of money (M) and lends it to companies (ordinary short-to-medium term loans). Subsequently, companies use the money for their production needs and, typically, to pay salaries: therefore, 80 M end up in profit to individuals, 20 M are available for the enterprise to make subsequent investments or are left as a reserve. This amount of idle money prevents achieving full employment due to the lack of corresponding investment. But this is where de-cumulation steps in. Let's take an amount of 5% to redress the balance: the proceeds of the stamps go to the central government, which then reinvests them to achieve full employment. Or to cover part of the expenses of its bureaucracy. The first option seems more realistic for the times in which stamped money was conceived, when most of the money was printed and the available financial instruments were limited compared to the current situation. Finally, enterprises, individuals and the central government spend their money and help balance the accounts at the central bank. The diagram above shows how Keynes and Gesell eventually converge toward a very similar model in which the government is tasked with making the system reach full employment through investment. It does not make very much a difference if investment is achieved through a deficit spending policy rather than using the proceeds from the stamps. Alvi shows how this approach to economic policy actually characterizes the historical period of the New Deal in America and the Nazi and Fascist regimes in Europe. It is worth reminding, however, that what normally passes for Keynesian policy, or support to investment with public money, was to remain an exceptional measure in the intentions of its author, to be implemented only in extreme conditions, such as those occurring near the onset of the so-called liquidity trap, i.e., in the presence of deflationary conditions. Although Keynes judged Gesell "a crank," Keynes agreed with the German merchant that money should be spent or invested and therefore that it was necessary to study a change of financial markets in order to obtain this result. The solution would later be proposed by Keynes as head of the British delegation to the Bretton Woods Conference in 1944: a supranational currency that de-cumulated, the Bancor, to balance foreign debts. But that's another story... The result of an investment policy based on national debt is now under the eyes of all. However, we must not believe that the stamped money is the solution to all evils. It was not possible to clearly see the limits of Gesell's construction due to the short life of its practical applications or other contingencies had. For example, the good mayor of Wörgl, Michael Unterguggenberger, noticed a possible inflationary drift of the money he had conceived, and remedied it in time by withdrawing a certain part of it from circulation. Gesell's money is indeed potentially inflationary. This is what Massimo Amato and Luca Fantacci write in this regard:

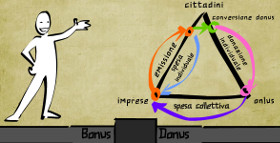

It must also be said that, without a regeneration of money, an economic body like Gesell's would eventually collapse on itself, and financial speculation would still be possible. While stamped money solves the problem of hoarding, because the burden of the stamp makes accumulating liquidity inconvenient, we need at least another kind of money that allows the business cycle to regenerate and stimulate growth. It is therefore a matter of extending Gesell's monetary model, introducing credit as a new type of real money, as would be explained much later, in the 1930s, by another great economist of the 20th century, Joseph Schumpeter. Steiner's three kinds of moneyWe have discussed stamped money in the section above and we have seen both its extraordinarily innovative aspects - one might say almost subversive compared to the current system - and the problematic aspects such as the possibility of speculation and the inflationary implications. To address these issues, Rudolf Steiner proposed a reform of money and financial markets in line with his vision of a social body organized into three independent spheres. These spheres correspond to the state, economic and cultural/spiritual domains. Here is the first important difference with respect to Gesell's model: money and the stamp are not managed by the government. It is not its job to issue money but it is the task of the economic sphere; the government is responsible for enforcing laws and ensuring national security both internally and externally. The issue of money lies therefore with private banks operating in a free banking system, that is in competition with each other without the monopoly of a central bank. In this scenario, Gesell's stamped money corresponds to Steiner's purchase money. Alvi calls this money mercor. Its de-cumulation generates a second type of money, Steiner's gift money that Alvi calls donor. Consistent with his vision of the three-fold commonwealth, even the stamp - or electronic withdrawal from a bank account or other de-cumulation mechanism - will not be collected by the government but issued and collected by all the institutions of the cultural sphere which, with the approval of the government, will have the legal power to issue it to sustain itself financially. The resources will be allocated among the various institutions according to the preferences freely expressed by citizens with the purchase of the stamps. The life of cultural institutions, therefore, will depend on people's actual understanding of their work, regardless of whether these are schools, universities, hospitals, theaters or music conservatories. Since none of these entities will no longer be run by the government, they will take the form of autonomous foundations. This will lead to a profound transformation in the government's redistribution mission. No longer a centralized redistribution conditioned by politics and implemented through general taxation, but rather a profoundly libertarian redistribution delegated to citizens, through a mechanism like today's 8 per thousand tax on income tax extended to all cultural institutions, constituting so to speak a mandatory gift but with freedom of destination. But the squaring of the circle is still missing from the picture. For Steiner, value is a holistic concept, it does not depend only on the interaction of the classic factors of production - land, labor and capital - but it is the result of two polarities, nature and spirit. That is to say, economic value is generated in two ways: by changing the nature of human work or changing work by means of the spirit. A position that emerges later also in the German sociologist Ferdinand Tönnies, who describes two different forms of social organization: the community (Gemeinschaft) and society (Gesellschaft). The former is pre-industrial and involves instinctive participation and a sense of belonging; the latter, typical of modern industrial society, is based on exchange and rationality. Value as the product of the Geist it expresses is the result of the relationship between nature and labour as a complex activity of a community; Geist takes on different meanings in German. It is the spirit but also rationality, intellectual capacity and even morality. It is the creative and visionary ability that leads the entrepreneur to innovate and produce. These issues were taken up later on by Joseph Schumpeter, an Austrian by birth, who later moved to the United States, in his original work "The Theory of Economic Development" of 1912. Schumpeter, like other economists, also recognized the tendency that an economic system has to achieve a general balance between endogenous factors (consumer desires, technological development) and exogenous factors (government, institutions, political movements and historical events). However, he also believed that this balance is static in nature (like that of Gesell's model) if it is not integrated, or rather broken by something else. It requires a dynamic element, a factor that disrupts the steady state through a creative manifestation of the Geist, an innovation that produces development and progress through the figure of the entrepreneur, whose spiritual abilities must be able to have access to the necessary financial resources. To allow the Geist to manifest this specific social function, Steiner postulated the need for loan money - called, in Alvi's terminology, invor. Loan money is reversed time, it is an anticipated future, which, through the financing of investment, makes it possible to produce goods, services and innovation, all of which are the fruit of the imaginative abilities of an entrepreneur. By analogy, Steiner also calls it young money. Through investments, the enterprise produces revenues with which to pay wages that become the spending power of households. 'Young money' is transformed into purchase money, and finally, through de-cumulation, into 'old money', gift money. The latter, received and spent by cultural institutions, eventually returns to where it started: the issuing banks, to be destroyed and to balance the circulation of money with the needs of trade, i.e., with the values of the goods on the market. Steiner's money is characterized by its two key moments, i.e., its birth and death. It is born from the freedom of issue and dies, through de-cumulation, giving itself to the Spirit, to the cultural sphere, which will give birth to a new idea that will attract the bank's money and materialize into a new business venture. It is worth noting that Steiner believed that it is legitimate to apply interest on loan money, being industrial credit. Steiner did not pursue any ideological crusade against interest; on the contrary, with a great sense of reality, he justified it linking it to a concept of reciprocity:

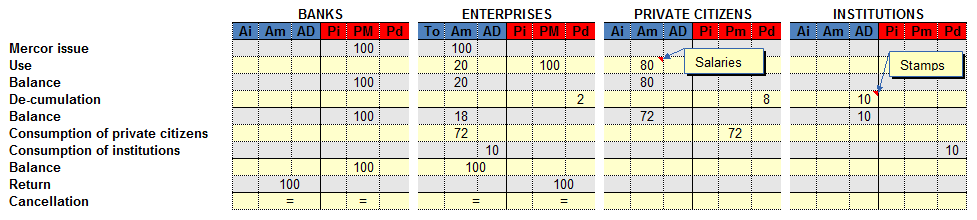

Therefore, let us review Gesell's scheme and then extend it to Steiner's. The scheme is complicated a bit by the fact that assets and liabilities must now take into account, not one but three kinds of money. The central bank disappears as the only issuer of money and in its place there are several independent institutions. The central government also disappears and is replaced by cultural/spiritual institutions. We will proceed step by step and, for educational purposes, we will present immediately the situation of Table 1 adding only household consumption (Tab. 2):

It should be noted in the header of the columns how the assets and liabilities are now split into three components: invor, mercor and donor (subscripts "i", "m", and "d" respectively). As per the scheme in Table 1, let's assume that banks lend - covered by cash assets or shares - 100 units of purchase money or mercor. The companies will use this money to produce goods and to pay wages and suppliers. Therefore, a share of 80 units will go to individuals while the remaining 20 will remain at the company as liquid reserves (intermediate balance line). The mercor is a Gesell-type money for which you have a periodic de-cumulation assumed here to be 10%. In this scenario, however, the stamps are issued by institutions of the cultural sphere; mechanisms for selecting the recipients of the gift - for example, along the lines of the 8 or 5 per thousand - will allow a smooth transformation of the purchase money into gift money, of the mercor into donor. To support these institutions, no further taxation is levied by the government. The government will collect the tax only when it is necessary to meet the costs of its representative bodies. The amount that is now available to individuals and institutions is used to meet their own needs, i.e., purchases of goods and services that carry 72 mercor in assets to individuals and 10 to institutions. The balance of 100 for the enterprises allows them to repay the initial issue of mercor and the cycle closes. It should be noted that the mercor always de-cumulates, whether it be in the bank or in one's own wallet; in the first case, if the money is not invested, it de-cumulates in the bank but if the account holder decides to lend and invest it, then the burden of de-cumulation is handed over to the debtor and the effect that the investor observes is the freezing of the de-cumulation of his own money. As seen in the previous paragraphs, however, if nothing else intervenes in the economic cycle, these would be the conditions of a Schumpeter-like static system. Its inertial evolution at every de-cumulation cycle could lead to the erosion of the wealth produced (see Tab. 3):

Without new investment, enterprises would eventually not be able to maintain the production levels achieved, which would be reduced progressively. Similarly, on the banks' side, there would be a corresponding depletion of resources linked to the return cycle of the money to be destroyed. In Steiner's diagram we have the fix: young money or investment money, also called invor by Alvi. The issue of this money can be understood as the issue of banknotes in exchange of movable assets (i.e., investments and securities) and real estate, or simple bank loans. In both cases, these are medium-term loans provided by banks either through the printing of new money or relying on the credit multiplier (secondary seigniorage) respectively. The issue of new money on the market will enable the production of goods and services. The scheme is changed as follows (Tab. 4):

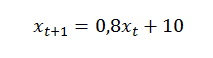

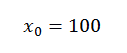

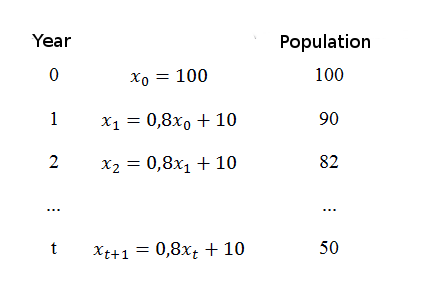

In the first line we find the balances relating to the inertial scenario above. This static situation can be overcome by the banks that issue 20 invor, anticipating the credit for investment to the enterprises. The revenue from the sale on the market of goods produced with the investment will be used to pay salaries, then generating the spending power of workers, or purchase money: the invor becomes mercor, which will be subject to the de-cumulation mechanism. However, let us proceed with order. Of the 20 invor, let's suppose that the enterprises use only 10 and 10 are returned to the banks. There will then be room for the creation of additional 10 mercor for enterprises. The invor are slower in becoming mercor than the mercor in becoming donors, because they are needed in more economic cycles of which they constitute an element of continuity and the real driving force. Steiner's money circulates in the true sense of the word since it comes back to where it started from. Present-day money, instead, spreads like wildfire, but it does not circulate, it often remains liquid and hence unproductive. This scenario needs to be supplemented by at least two considerations. The first concerns the problem of the possibility of speculating even with a money that de-cumulates like present-day money. This aspect had already emerged when discussing of Gesell's money. Steiner's money does not preclude this possibility. For this reason, it must be accompanied by a major overhaul of financial markets. In the stock exchanges we know today, only a small fraction of transactions - perhaps no more than 3% - actually goes into increasing the share capital of enterprises. The rest is pure speculation: shares are bought and sold making a profit on margins, but not a penny goes to businesses. Only when the institutions responsible for raising capital will act consistently with those that have been described here, such as investment banks, will capital be able to act healthily within the economic body. This gives rise to another problem that leads us directly to a second set of considerations. If speculation is no longer the main reason that actually guides the choices of investors, how should they orient their preferences? Should investment banks alone provide for this function? Whenever Rudolf Steiner spoke about social issues and economics, he never failed to point out that a healthy evolution of the economic sphere would necessarily lead to an associative economy. By this he meant an economy in which associations of operators involved in the production, circulation and consumption of goods would be established. Only the activity of these associations would make it possible to fully and consciously develop what the theories of classical economists called the invisible hand. Rather than letting the market regulate itself independently, assuming that it is capable of doing so, the associations coordinate production, circulation and consumption bringing out the real needs of human communities; and financial institutions, in collaboration with them, contribute for their part in the creation of a "conscious market". Whether or not a bank should fund an entrepreneur will depend on whether what he intends to accomplish is actually a need clearly expressed by the complex relationships that emerge from the associations. It is not a centrally planned economy like that purported by real socialism. It is well known that in the thought of the Austrian philosopher the central government is completely excluded from issues concerning the economic sphere. Rather, in this scenario, investment banks, moving in tune with the associations, put their trust in projects and entrepreneurs not on the basis of mere profit maximization, but above all on the ability of a project to meet a specific social need. There will no longer be any need for market surveys, or worse, for the artificial creation of certain needs that people do not really have. Banks will definitely be able to assess business risk better than they do today, since the size of the initiative to be funded will be commensurate to the feedback from the associations. Banks will have to regain the ability to evaluate first and foremost ideas and their carriers. Today they deceive themselves into believing that they manage business risk hedging it mechanically with mortgages and guarantees; tomorrow they will have to gain a deeper business insight and foster initiatives that the community needs [5]. Banks will almost become the organs of perception of the associations to find the ideas of those entrepreneurs who can meet the needs of the community. For example, if a given territory needs a certain amount of wood, enterprises active in this sector will not be able to be more than those actually needed to meet domestic demand. If an entrepreneur were to establish nonetheless a new business operating in this sector, the associations in the area would inform the investment banks that local needs actually require resources for other purposes. The associations could urge to establish a local business to avoid having to buy part of the wood from distant companies and hence the resulting environmental damage caused by transport. They might decide instead to buy the wood from elsewhere to preserve a certain territory and its unique biodiversity. In any case, only the real needs would come to the surface and the economic sphere would fulfill the task of meeting human needs by adapting to them. Only in this way can a truly sustainable economy be born from the current situation. The evolution of invor, mercor and donor in timeIn the paragraphs above we discussed how the transformation of mercor into donor is a process that requires some time to take place. The available mercor, however, never succeeds in becoming entirely donor. At each temporal iteration, the catabolic de-cumulation of mercor is compensated by the anabolic process of the creation of invor. But how do these three kinds of money evolve in time? For example, is there a risk that a "wrong mutual setting" of the rate of investment and de-cumulation may have a combined effect of making the monetary system as a whole completely unstable? Is it possible to mathematically model the relationships between these variables and study their evolution over time? Recourse here to the science of numbers is not a way of surrendering to the deplorable contemporary tendency of economics to apply mathematics to everything. In fact, we will see that with this help we will be able to reach conclusions that may help us achieve a better understanding of the object of this study. However, for those who have never had a liking for the noble science of numbers, it is possible to skip to the next chapter and the conclusions presented in the following one. Discrete dynamic systemsThe relationship between the three kinds of money, as can be seen in the diagram above, can also be stated as follows: in the monetary system, at a given instant, the amount of mercor present is equal to the amount of mercor present the instant before minus the de-cumulated mercor plus a certain amount of invor. This relationship is a typical example of the problems that are addressed by a branch of mathematics that studies how different quantities (which taken together constitute a system) evolve (dynamic system) over a period of time that is not observed continuously but at set intervals. Namely, it is a discrete dynamic system. As complicated as the evolution of the system as a whole may be, the evolution from a certain instant to the next is determined only by a recursive law. For example, in a certain valley in the Alps 100 mountain goats are introduced to repopulate the habitat from which they had disappeared long ago. Every year 20 die while 10 mountain goats are born. How does this population evolve over time? Will it disappear, grow or remain constant? We are trying to understand how it evolves:

that is

for the first year, however, we know how many heads compose the initial population, which at instant zero, is:

Then the evolution in time will be:

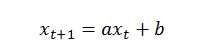

We can easily see that the population will stabilize at a level of 50 animals over the years. The generic law shown above for time t+1 is called difference equation and in this specific case, it takes the general form of:

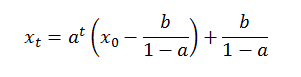

it is also called affine linear equation. For this class of equations, the solution that identifies the balance of the system - which can be stable, unstable or constant - is described by:

It is easy to see that when 0 < a < 1 as at tends to zero, the system always has a stable equilibrium in b/(1-a) and for any value of x0 (ergodic system). This result essentially tells us that an affine linear system characterized by a percentage decrease accompanied by an absolute increase, always tends toward a state of equilibrium and is therefore stable. In other words, if we want resource x not to deplete over time, we should not take a constant amount of it at each interval of time, but a certain constant percentage. Based on this mathematical theory, let's now apply it to Steiner's three kinds of money. The relationship that describes the evolution in time of the amount of mercor is the following:

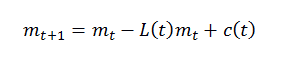

that is, the amount of mercor at time t+1 is given by the amount present at time t less a de-cumulation L (function of time t) plus a quantity c, it too a function of time t. Let's have a closer look at these quantities:

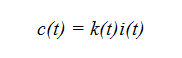

c(t) is given by the evolution in time of the invor i(t) as investment k(t) varies over time. For the sake of simplicity, let's assume that investment is constant over time, i.e., that c(t) is constant, so c(t) becomes C. The function L(t) that describes de-cumulation in time can be considered constant and comprised between 0 and 1. So we have:

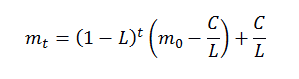

an ergodic affine linear equation whose solution is:

of which we are now ready to study the evolution in time. Stability of the mercor, invor and donor systemBefore beginning to study the behavior of Steiner's three type of money over time, let's consider the most relevant entities involved:

Mathematical theory tells us that the constant C/L represents the equilibrium point of the system, i.e., the value the mass of mercor tends to over time. Let's see now the first simulation using this data:

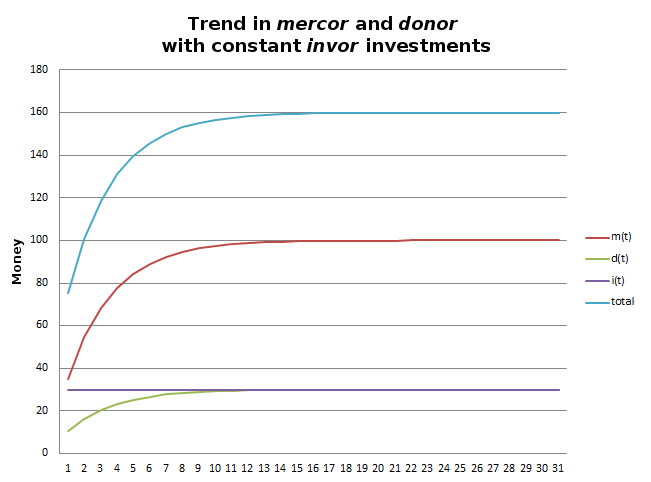

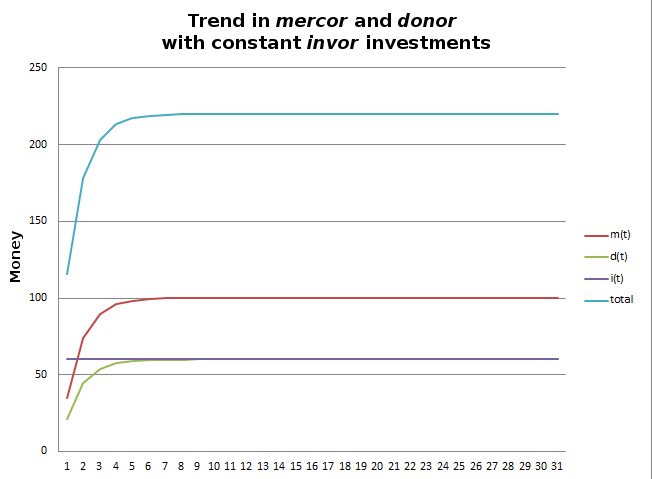

That is, the arbitrary initial amount of mercor is equal to 35, 30% of de-cumulation and constant investment of invor is equal to 30. As seen in Fig.1, the equilibrium point of mercor is reached at 100, the total mass of money in the system is 160 and the donor tends to match the investment of invor:

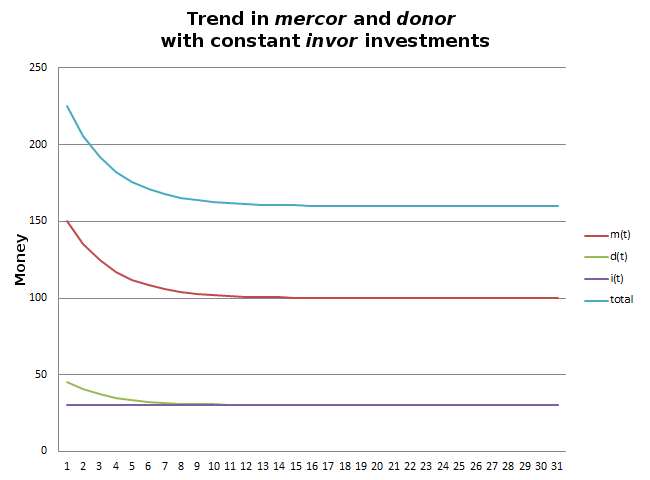

Let's see what happens if we increase the initial amount of mercor bringing it to a value higher than the equilibrium point:

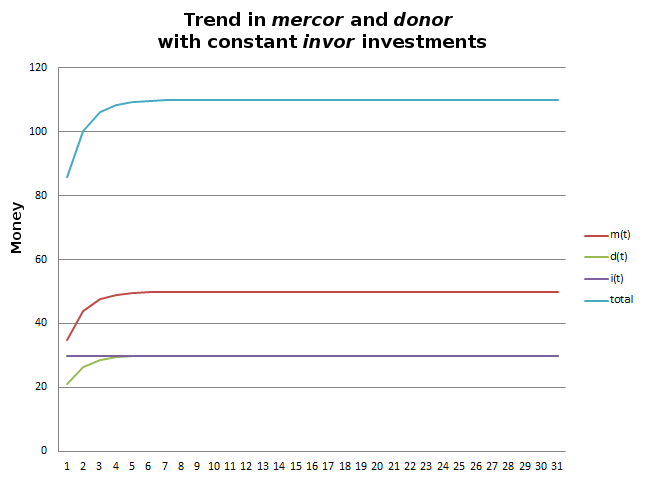

In Fig. 2 we see how the system still reaches the equilibrium point at 100 and the mathematical theory assures us that this will happen regardless of the initial value of the mercor. At this point let's see a more interesting simulation. Let's suppose that we are in the initial situation described in Fig. 1. It should be observed that the social body as a whole, in these conditions, actually experiences a certain degree of suffering in the cultural sphere. The institutions of this sphere, like schools, hospitals, theatres, foundations, etc., suffer from a blatant lack of funds. This poses the problem of how to act on the system in order to provide more donor to the cultural sphere. You might consider modifying the size of the de-cumulation by doubling it to 0.6. However, it is easy to notice that by doing so the equilibrium point is lowered to 50:

If we look now at the new graph, perhaps with some surprise, we find the situation described in Fig. 3:

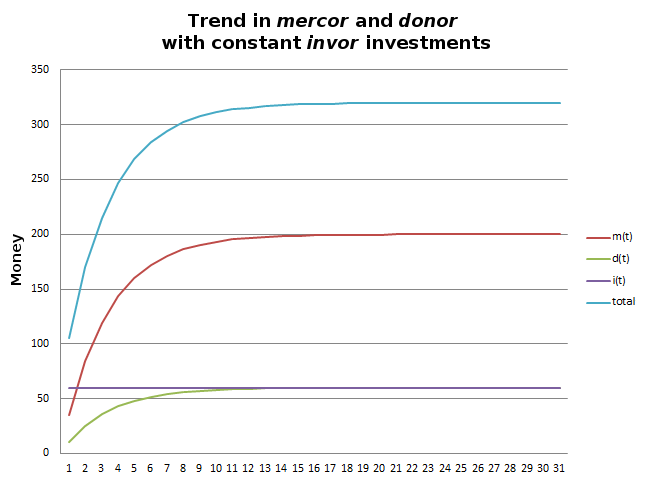

What we have achieved in actual fact is not an increase in the amount of donor but a contraction of all the circulating money. The doubling of de-cumulation has caused a strong and rapid drain of mercor. Indeed, we can see that the new equilibrium is reached with fewer temporal iterations compared to the simulation in Fig. 1. So we have certainly learned the lesson. If we want more donor, we have to leave everything unchanged and double investment. The equilibrium point, however, is reached at a value double the previous one:

If we look at Fig. 4, in the new scenario we have succeeded in our aim of doubling the donor, while causing a doubling of mercor and a corresponding increase in circulating money

At this point the correction would seem trivial. To maintain the value of the circulating money constant with the aim of increasing the donor, the optimal configuration in theory is the following:

The situation now is the one described in Figure 5. This means that an improvement in the cultural sphere, without changing the amount of mercor, can only be achieved with the concomitant increase in de-cumulation and investment. Compared to the previous situation, we must not lose touch though with the economic reality. The transformation of the invor into mercor is mediated by economic processes that do not allow reaching this hasty conclusion. For example, it might be true only in an ideal world in which greater investment is matched exclusively by higher revenues, and higher wages, that is mercor to be spent. But this does not happen for example for those investments that optimize production resulting in less staff. In addition, the aggressive pursuit of increased investment and therefore a hypertrophic increase in production is not sustainable in the long term for environmental reasons. In this scenario, it would be necessary to take action in multiple directions, with new and more productive technologies, cutting costs, etc., that is to say, providing the social body precisely with those talents and abilities that are the result of a sound and adequately supported cultural sphere. And all this should take place in a sustainable environment avoiding the depletion of the planet's resources.

Projects and current applicationsWe saw earlier in the Wörgl experiment that it was the Austrian central bank to order its end by declaring the new currency created by the mayor of the Tyrolean village to be illegal. In essence, it was claimed that the law by which only the central bank can issue currency had been violated. Today, the situation is no different, although there are many complementary or local currencies, even in Italy, that circulate alongside the main currency. Not all of them are actually money; some are simply discount mechanisms accepted on a voluntary basis or other mechanisms based on barter or the exchange of services. Usually, not having any major impact on the circulation of the official currency, they are tolerated by central banks and are sometimes the object of accurate tax audits in order to avoid possible scams against the treasury. In general, it is unlikely that further experiments like the Wörgl experiment can be extended significantly: as soon as there would be news of a similar effort, the central banks would definitely go from tolerance to repression. Aware of this limitation, these initiatives have at least the merit of yielding some benefit to the circulation of money in a given territory and above all convey a new and healthier concept of money. Among the current applications or plans of complementary perishable money, the following are the ones that in our opinion are the most significant. The Chiemgauer

But what is the life cycle of this complementary currency? To enter the circuit, all you need to do is contact one of the many "bureaux de change" in the area and change euro for chiemgauer. The exchange rate is €1 = CH 1. By way of guarantee for those participating in the circuit, the issue of the local currency is hedged by a corresponding bank deposit in Euros. At this point you can use the Chiemgauer whether you are a producer or a consumer: you can use it to pay employees, or purchase goods and services in any business that accepts the currency. Every three months, you need to apply a stamp worth 2% of the nominal value of the Chiemgauer banknotes to keep them valid (i.e., 8% on an annual basis). The proceeds from the sale of the stamps go to non-profit associations according to the preferences expressed by their buyers. This fee ensures that the Chiemgauer can circulate three times faster than the euro. When you need to change Chiemgauers into euros, you apply a 5% rate. Of this 5%, 2% goes to the cooperative that issued the money to cover the operating costs, while the rest goes to non-profit associations registered with the association. From the fiscal point of view, the Chiemgauers are treated like the official currency so that they are taxed in the same way (shops that use it issue invoices to the cooperative). The Libra ProjectThe "Libra Project" was launched as a concrete effort to be achieved by an "organizing committee of the foundation for gift money" established in Milan in 2001. The committee has the task of creating "the technical, legal and fiscal conditions for the construction of complementary currency systems". The result is an exchange and gift circuit that is based on a social complementary currency. Here's how the circuit works:

The mechanism seems quite similar to that of the Chiemgauer, but it makes use of electronic cards for the management of the points. The convenience for retailers participating in the circuit is the promotion of loyalty among consumers who choose their products instead of others, vis-à-vis their funding of the donus. The success of this initiative depends very much on whether the actual cost incurred by traders is lower than what they currently spend in advertising and marketing or, more generally, if the offered discount ultimately has a more profitable return. The only drawback of the project: it seems to have been suspended at least there seem to be no recent updates on the website. We hope that the initiative will soon be resumed entering the implementation phase proper. ConclusionsThe Wörgl experiment came to an end as soon as the neighboring villages also showed their interest in copying the initiative of the money that "alleviates need, provides bread and work". This would seem the inevitable denouement of these initiatives: as soon as the monopoly over the issue of money appears to be seriously in danger, the central bank changes rapidly from a tolerant stance to a repressive one and the experiment is terminated. One might then ask how a reform of money like the one described here can ever hope to be achieved. It is useless to expect that it can be imposed from above, considering the interests existing between the political and economic sphere. However, it is this very limit of the territorial extension of complementary currencies that could prove to be a positive factor in determining the future success of demurrage money. Other economic and social symptoms that can already be seen clearly around us seem to point to a possible virtuous transformation of current conditions. Undoubtedly in recent years, ethical banks, microcredit and ethical investments have gained growing importance. There is an increasing number of companies that incorporate ethics in their business models in various ways. For example, some companies have adopted a special legal framework in managing issues relating to company ownership. Others rely on foundations to support cultural institutions, schools or other bodies belonging to the world of culture, or join in groups of businesses to better manage their ethical interests, etc. These companies almost appear to be like "pioneer plants" in the desolate economic and social landscape that is all around us. They are preparing the social ground with a new awareness so that new relationships can flourish through them both inside and outside their companies. Among these innovative relationships, co-creative approaches between businesses and consumers are without doubt the most interesting and promising. Although in many cases they are nothing more than sophisticated forms of marketing, it is nonetheless possible to catch a glimpse of the germs of future associations of consumers and producers. These initiatives typically lack geographical connections. But as their numbers increase, they can finally create small communities (comprising few municipalities at the beginning) based on an entirely new concept of the role of the social body in the economic sphere. A broader and deeper social awareness will finally encourage the creation of a complementary perishable currency in that circumscribed area to support the cultural realities within it. These narrower territorial entities can then join together to reach the critical mass necessary for an effective large-scale transformation. Notes:[1] Hans Georg Schweppenhäuser “Das Kranke Geld” - Fischer Taschenbuch Verlag - 1982 [2] References can be found in “Le seduzioni economiche di Faust” - Adelphi – 1989. “L'anima e l'economia” - Mondadori 2005 - the chapters at p. 296 “La teoria del valore di Rudolf Steiner” and p. 307 “invor, mercor, donor: i tre denari” quote what was already published in the journal “Trasgressioni” in the issue of January-April 1997. “La Confederazione italiana” - Marsilio Editore 2013 – Chapter 29, “Per una moneta che nasca, viva e muoia”. [3] Who held the currency could hand it over to the mint, have it molten and receive good money but just by paying a percentage on the coinage, a tax that was also called seigneurage, from which today's seigniorage, i.e., the profit that goes to the entity that coins money (also called primary seigniorage) [4] Avigliano went on to publish a second book in 1926, "L'enigma sociale", which studies more in detail perishable money. [5] Today Islamic banks operate in a very similar way. Since they cannot grant interest-bearing loans to follow the precepts of the Koran, they develop partnerships with businesses to take part of in their profits and recover the costs. They also share the risks and have an interest in making sure that the company prospers. For further information on the topic:

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The seventh of nine children, Gesell was born in 1862 in Sankt Vith, a town belonging at the time to the Rhine Province of the German Empire and now a part of Belgium since 1919. His parents wanted him to go to university, but Silvius never did: the death of his father forced him to leave school and take a job as a clerk in the postal service of the German Empire. He did not stay for long. Shortly after he resigned to go into business as an salesman of his brother's company that sold dental materials. He first moved to Malaga, Spain, and in 1877 to Buenos Aires. Argentina was for Gesell a theater of experiences that profoundly affected him and would go on to provide the living material from which

he would draw conclusive evidence in support of his later economic thinking. In 1890, in fact, the speculative bubble burst, triggered by Baring Brothers, the oldest merchant bank in London, older still than the bank of the Rothschild family. Baring, favored by the lucrative financial conditions created by the Argentine government, had managed to funnel a huge share, almost 50%, of British foreign investment to Argentina until an Argentine water utility could no longer honor its payments causing a chain reaction that resulted in the bubble's burst. The City's banks, including the Bank of England, ran for cover, bailing out Baring Brothers to cover its exposure in order to prevent even worse trouble for the entire financial system. In Argentina, the situation became dramatic: the flight of foreign

capital, and the rise in interest rates led the country to collapse. Commodity prices began to fall prompting consumers to delay purchases because they were certain of future declines. The goods remained unsold, businesses went bankrupt one after the other, and unemployment soared. In short, deflation had come.

The seventh of nine children, Gesell was born in 1862 in Sankt Vith, a town belonging at the time to the Rhine Province of the German Empire and now a part of Belgium since 1919. His parents wanted him to go to university, but Silvius never did: the death of his father forced him to leave school and take a job as a clerk in the postal service of the German Empire. He did not stay for long. Shortly after he resigned to go into business as an salesman of his brother's company that sold dental materials. He first moved to Malaga, Spain, and in 1877 to Buenos Aires. Argentina was for Gesell a theater of experiences that profoundly affected him and would go on to provide the living material from which

he would draw conclusive evidence in support of his later economic thinking. In 1890, in fact, the speculative bubble burst, triggered by Baring Brothers, the oldest merchant bank in London, older still than the bank of the Rothschild family. Baring, favored by the lucrative financial conditions created by the Argentine government, had managed to funnel a huge share, almost 50%, of British foreign investment to Argentina until an Argentine water utility could no longer honor its payments causing a chain reaction that resulted in the bubble's burst. The City's banks, including the Bank of England, ran for cover, bailing out Baring Brothers to cover its exposure in order to prevent even worse trouble for the entire financial system. In Argentina, the situation became dramatic: the flight of foreign

capital, and the rise in interest rates led the country to collapse. Commodity prices began to fall prompting consumers to delay purchases because they were certain of future declines. The goods remained unsold, businesses went bankrupt one after the other, and unemployment soared. In short, deflation had come.  “Lindert die Not, gibt Arbeit und Brot” (It alleviates need, provides employment and bread) wrote mayor Unterguggenberger about his currency. Paradoxically, it was the realization of this promise and the consequent enthusiastic spread of his experiment that marked its end. Unterguggenberger died of tuberculosis in 1936 in Wörgl.

“Lindert die Not, gibt Arbeit und Brot” (It alleviates need, provides employment and bread) wrote mayor Unterguggenberger about his currency. Paradoxically, it was the realization of this promise and the consequent enthusiastic spread of his experiment that marked its end. Unterguggenberger died of tuberculosis in 1936 in Wörgl.

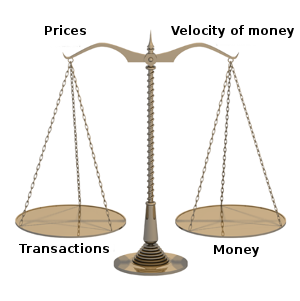

The idea of monetary de-cumulation is certainly correct but incomplete. The problem is two-fold. On one hand, in Gesell's scheme the government issues the currency and stamps. In theory, a virtuous central bank capable of properly handling the relationship between issue, circulation and de-cumulation should not trigger inflationary processes. In practice, a monetary system subservient to politics and used in varying degrees to pay for the favors and profits of the patronage supporting it will invariably result in inflation. This topic was also investigated by the aforementioned American economist Irving Fisher, who was extremely interested in Gesell's money. Fisher devised

an equation that models the relationship between the quantity of goods in circulation and their price on the one hand and the quantity of money and its velocity of circulation on the other and imagined it as a sort of scale. The quantity of goods available on the market would be put on one side of the scale and the amount of money in circulation on the other, while their arms represented the price level and the velocity of money. It is the so-called "equation of exchange", where the variation of one of the items makes the others tend immediately to recover a state of equilibrium. So, for example, if the money supply or the velocity of money increases, without any change in trade needs, the system responds by lengthening the arm that marks the price level, resulting in inflation. The

de-cumulated money, by its very nature, leads to a rise in the velocity of exchange, triggering distortions in the system of the relative prices, with inflationary consequences.

The idea of monetary de-cumulation is certainly correct but incomplete. The problem is two-fold. On one hand, in Gesell's scheme the government issues the currency and stamps. In theory, a virtuous central bank capable of properly handling the relationship between issue, circulation and de-cumulation should not trigger inflationary processes. In practice, a monetary system subservient to politics and used in varying degrees to pay for the favors and profits of the patronage supporting it will invariably result in inflation. This topic was also investigated by the aforementioned American economist Irving Fisher, who was extremely interested in Gesell's money. Fisher devised

an equation that models the relationship between the quantity of goods in circulation and their price on the one hand and the quantity of money and its velocity of circulation on the other and imagined it as a sort of scale. The quantity of goods available on the market would be put on one side of the scale and the amount of money in circulation on the other, while their arms represented the price level and the velocity of money. It is the so-called "equation of exchange", where the variation of one of the items makes the others tend immediately to recover a state of equilibrium. So, for example, if the money supply or the velocity of money increases, without any change in trade needs, the system responds by lengthening the arm that marks the price level, resulting in inflation. The

de-cumulated money, by its very nature, leads to a rise in the velocity of exchange, triggering distortions in the system of the relative prices, with inflationary consequences.

Chiemgauer is the name of a local perishable currency that was initially created in 2003 as a simple school project developed by Christian Gelleri, a teacher at the Waldorf school in Prien in the Chiemgau area near Munich. Pretty soon, given the promising developments, the project spread outside the school to give rise to a cooperative which now has 3000 members, 600 companies and 250 non-profit associations, with a circulation of about CH 3 million (chiemgauer).

Chiemgauer is the name of a local perishable currency that was initially created in 2003 as a simple school project developed by Christian Gelleri, a teacher at the Waldorf school in Prien in the Chiemgau area near Munich. Pretty soon, given the promising developments, the project spread outside the school to give rise to a cooperative which now has 3000 members, 600 companies and 250 non-profit associations, with a circulation of about CH 3 million (chiemgauer). The Libra circuit is an exchange circuit between citizens, businesses and non-profit organizations. The companies participating in the circuit have the right to give their customers electronic points called bonus (let's say they are equal to 10% of the price). Points can also be given to employees as salary bonuses and in general as part of a policy of company incentives. For example, they are proportional to the amount of a purchase and are linked in general to promotional campaigns. The bonuses that the citizen gets from the various businesses are accumulated in a single personal e-wallet. The accumulated bonus points can be used to

purchase goods and services from any firm participating in the circuit. Unspent bonus points are progressively transformed into other kinds of points. Periodically, a certain percentage of the bonus balance is converted into donus. The donus are kept by citizens in the same e-wallet but unlike the bonus they cannot be spent at the participating businesses. They can only be donated to non-profit organizations belonging to the circuit. Citizens are free to choose from time to time the organization of the circuit they wish to donate their points to. Non-profit organizations can spend their donus at all the businesses of the circuit. If they do not spend the donus in a year, they will be distributed among the other associations according to established

criteria. Meanwhile, the bonus points that are not converted into donus continue to be spent by the citizens. For example, if a citizen receives 13 bonus points obtaining goods and services worth 11 euros, donating 2 euros, the non-profit organization has received and spent 2 donus getting goods and services worth 2 euros. The businesses have donated goods and services that are worth 13 euros for the citizens and organizations but that cost less to the businesses. The bonus points and donus collected by the businesses can be re-assigned to citizens as a bonus so that the circuit is constantly restarted with economic benefits for each individual and benefits to society as a whole.

The Libra circuit is an exchange circuit between citizens, businesses and non-profit organizations. The companies participating in the circuit have the right to give their customers electronic points called bonus (let's say they are equal to 10% of the price). Points can also be given to employees as salary bonuses and in general as part of a policy of company incentives. For example, they are proportional to the amount of a purchase and are linked in general to promotional campaigns. The bonuses that the citizen gets from the various businesses are accumulated in a single personal e-wallet. The accumulated bonus points can be used to

purchase goods and services from any firm participating in the circuit. Unspent bonus points are progressively transformed into other kinds of points. Periodically, a certain percentage of the bonus balance is converted into donus. The donus are kept by citizens in the same e-wallet but unlike the bonus they cannot be spent at the participating businesses. They can only be donated to non-profit organizations belonging to the circuit. Citizens are free to choose from time to time the organization of the circuit they wish to donate their points to. Non-profit organizations can spend their donus at all the businesses of the circuit. If they do not spend the donus in a year, they will be distributed among the other associations according to established

criteria. Meanwhile, the bonus points that are not converted into donus continue to be spent by the citizens. For example, if a citizen receives 13 bonus points obtaining goods and services worth 11 euros, donating 2 euros, the non-profit organization has received and spent 2 donus getting goods and services worth 2 euros. The businesses have donated goods and services that are worth 13 euros for the citizens and organizations but that cost less to the businesses. The bonus points and donus collected by the businesses can be re-assigned to citizens as a bonus so that the circuit is constantly restarted with economic benefits for each individual and benefits to society as a whole.